Command Palette

Search for a command to run...

إحصاءات أساسية للمبتدئين

الملخص

Please provide the title and abstract you would like me to translate.

One-sentence Summary

By reformulating semi-parametric inference for time-changed Lévy processes from low-frequency observations as a composite function estimation problem, this study develops a composite characteristic function estimation method that yields consistent Lévy density estimates with uniform and pointwise minimax-optimal convergence rates, with algorithm performance validated through simulations on time-changed Normal Inverse Gaussian processes.

Key Contributions

- A consistent estimation procedure is developed for the Lévy density of a multidimensional Lévy process using low-frequency observations of its time-changed counterpart, leveraging the established connection to composite function estimation.

- The analysis derives uniform and pointwise convergence rates for the estimator and proves that these rates achieve minimax optimality over suitable classes of time-changed Lévy models.

- A simulation study on time-changed Normal Inverse Gaussian Lévy processes empirically demonstrates the performance of the proposed estimation algorithm.

Introduction

Financial modeling increasingly relies on time-changed Lévy processes to capture complex market dynamics like volatility clustering, yet parametric assumptions often introduce significant misspecification bias. While high-frequency statistical methods have advanced jump estimation, they struggle with real-world low-frequency data where jumps remain unobservable and increments exhibit dependence. To address this gap, the authors leverage composite characteristic function estimation to develop a nonparametric framework that recovers the underlying Lévy density directly from low-frequency observations. They prove the estimator achieves optimal minimax convergence rates and validate the approach through simulations on Normal Inverse Gaussian processes, providing a robust and flexible alternative to traditional parametric modeling.

Dataset

-

Dataset Composition and Sources: The authors work with synthetic time series data generated from multivariate time-changed Lévy processes. Observations consist of discrete increments Zj=YΔj−YΔ(j−1) for j=1,…,n, where each sample captures the process state at fixed intervals Δ.

-

Key Details and Filtering Rules: The data is structured across d components, each governed by a Lévy density νk. Rather than applying empirical filters, the authors enforce theoretical constraints: densities must belong to the Blumenthal–Getoor class Bγ with γ>0 to ensure infinite jump activity, possess finite absolute moments of order p>2, and satisfy specific tail decay conditions for the associated time change. Cross-component dependence is explicitly modeled, with misspecification bias bounded by the diffusion correlation Σ(k,l).

-

Data Usage and Processing Pipeline: The dataset feeds into a three-step estimation procedure. First, empirical characteristic functions and their partial derivatives up to third order are calculated. Second, the second derivative of the characteristic exponent is derived using ratio-based estimators that adapt based on a threshold κ/n. Third, a regularized Fourier inversion is applied to recover the Lévy density, employing a kernel K supported on [−1,1] and a decaying bandwidth sequence hn.

-

Structural and Analytical Framework: Instead of traditional cropping or metadata tagging, the methodology relies on local smoothness classes Hs(x0,δ,D) to evaluate pointwise convergence. The authors derive almost sure uniform convergence rates under global smoothness assumptions Sβ, dynamically adjusting the bandwidth hn based on the jump activity index γ and the tail behavior of the time change process Laplace transform.

Method

The authors present a method for estimating the Lévy density of a time-changed Lévy process, focusing on the estimation of the second moment of the Lévy density, denoted as νˉk(x)=x2νk(x), where νk(x) is the Lévy density of the k-th component process. The framework relies on the characteristic function of the observed process Yt=LT(t), where Lt is a d-dimensional Lévy process and T(t) is a nondecreasing time change process. The estimation procedure is based on the characteristic function of the increment Z=YΔ, which is given by ϕZ(u)=E[exp(iu⊤Z)]=LΔ(−ψ1(u1)−⋯−ψd(ud)), where ψk(u) is the characteristic exponent of the k-th component Lévy process and LΔ is the Laplace transform of the time change T(Δ).

The core of the method involves recovering the second derivative of the characteristic exponent, ψk′′(u), which is linked to the Fourier transform of νˉk(x) through the relation F[νˉk](u)=−ψk′′(u). This is achieved by exploiting the relationship between the derivatives of the characteristic function ϕZ(u) and the characteristic exponents ψk(u). Specifically, the authors derive identities that express ψk′′(u) in terms of the derivatives of ϕZ(u) and the characteristic exponent of a non-degenerate component Ltl. These identities, presented in equations (3.5), involve ratios of derivatives of ϕZ evaluated at specific vectors u(k), which isolate the k-th component. The derivation assumes the diffusion volatility σk is known, and the identifiability of the model relies on the assumption that the process Ltl is non-degenerate.

The estimation process begins with the construction of an estimator ψk(u) for ψk(u), which is defined as a normalized integral of the ratio of the empirical characteristic function derivatives. This estimator is then used to obtain an estimate for ψk′′(u) via the derived identities. The final step involves applying a regularized Fourier inversion to estimate νˉk(x) from the estimated ψk′′(u). The method also addresses the case of unknown diffusion volatilities by considering higher-order derivatives of the characteristic exponent, such as ψk(4)(u), which is related to the Fourier transform of νk(x)=x4νk(x).

The theoretical analysis of the method involves proving the consistency and convergence rates of the proposed estimators. The authors establish pointwise convergence rates by bounding the deviation between the true function νˉk(x) and its estimator νk(x), which is decomposed into a stochastic term and a bias term. The stochastic term is analyzed using a representation involving the difference between the empirical characteristic function and its expectation, which is bounded using a proposition on large deviations for weighted sup norms. This proposition provides concentration bounds for the supremum of the difference between the empirical and theoretical moments, which are crucial for controlling the stochastic error. The bias term is bounded using the smoothness properties of the Lévy density and the regularization kernel. The overall framework ensures that the estimator achieves optimal convergence rates under suitable assumptions on the smoothness and tail behavior of the Lévy density and the time change process.

Experiment

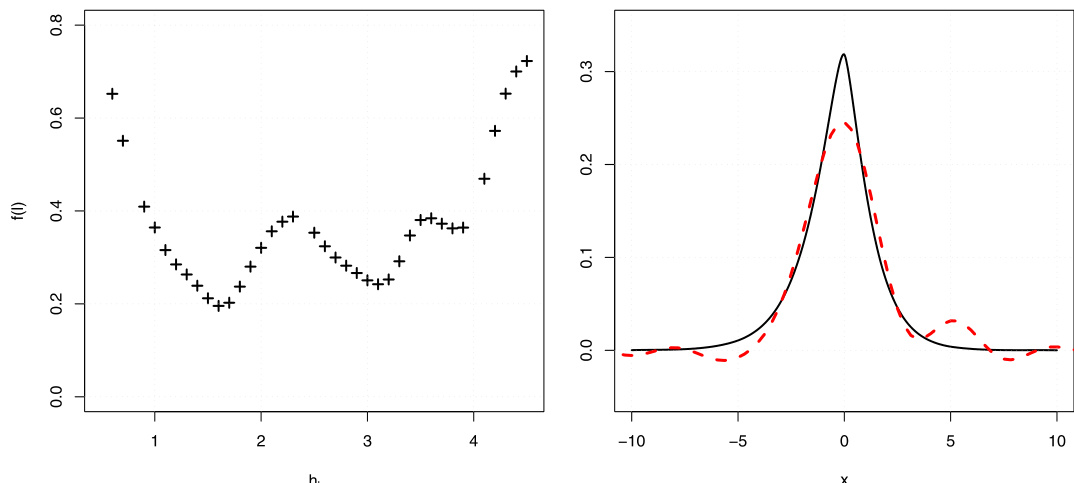

The evaluation employs simulation studies of time-changed Normal Inverse Gaussian processes using both Gamma and integrated CIR time-change mechanisms to test the finite-sample performance of an adaptive Lévy density estimator. By applying a quasi-optimality bandwidth selection strategy, the experiments validate how accurately the algorithm recovers the true underlying density across varying model parameters and sample sizes. The results demonstrate that the method consistently yields reasonable approximations, maintaining robust performance across different configurations and degrading only predictably as sample sizes decrease, which confirms its practical utility for modeling complex stochastic processes.

The authors analyze the convergence rates of an estimator for the Lévy density in time-changed Lévy processes, focusing on two types of time changes: a Gamma process and an integrated CIR process. The convergence behavior depends on the properties of the underlying Lévy process and the time change, with different asymptotic rates observed for cases where the mean of the Lévy process is positive versus zero. The results show that the convergence rates are generally slow, especially for polynomially decaying time changes, but the proposed estimation method performs reasonably well in finite samples. Convergence rates for the Lévy density estimator depend on the mean of the Lévy process, with different asymptotic behaviors observed when the mean is positive versus zero. The convergence rates are generally slow, exhibiting logarithmic or polynomial decay, and are influenced by the properties of the time change and the underlying Lévy process. The estimation method demonstrates reasonable performance in finite samples, as shown by the adaptive estimates and their ability to recover key functionals of the Lévy density.

The study evaluates a statistical estimator for the Lévy density within time-changed Lévy processes, specifically examining Gamma and integrated CIR time changes to validate convergence behavior under positive and zero mean conditions. The analysis reveals that asymptotic convergence is inherently slow, typically following logarithmic or polynomial decay patterns dictated by the interaction between the time change mechanism and the underlying process. Despite these theoretical limitations, the proposed method demonstrates robust finite-sample performance, successfully recovering key density functionals through adaptive estimation techniques. Ultimately, the findings confirm the estimator's practical utility while underscoring the persistent challenges of slow convergence in complex stochastic modeling.