Command Palette

Search for a command to run...

IEEE 不正検出コンペティション

概要

One-sentence Summary

Using a cross-sectional survey with structured questionnaires from Nigeria’s five largest licensed banks and an Ordered Logistic Regression model, this study determines that top management support, IT infrastructure, regulatory compliance, staff competency, and perceived effectiveness accelerate AI-driven fraud detection adoption, whereas high implementation costs discourage uptake.

Key Contributions

- This study integrates technology acceptance and fraud prevention determinants into a unified analytical framework to empirically identify the key factors driving the fragmented adoption of AI-driven fraud detection systems in Nigerian banks.

- It applies an Ordered Logistic Regression model to structured survey data from five major licensed banks to quantify how top management support, IT infrastructure, regulatory compliance, staff competency, and perceived effectiveness accelerate system uptake.

- The analysis identifies high implementation costs as a primary deterrent while confirming the significant impact of the five identified drivers, thereby providing actionable recommendations for executive training, scalable IT investment, and regulatory guideline development.

Introduction

The Nigerian banking sector faces escalating financial fraud risks as digital transactions surge, making AI-driven detection systems critical for maintaining operational security and regulatory compliance. Prior approaches relying on rule-based mechanisms prove insufficient against sophisticated cyber threats, while existing literature often overlooks the specific infrastructural and regulatory barriers hindering AI adoption in developing economies like Nigeria. The authors leverage the Diffusion of Innovation theory to empirically analyze the extent of AI adoption in Nigerian banks, identifying cost, compliance, and competency as primary determinants while proposing a unified framework to guide strategic implementation and policy development.

Dataset

- Dataset Composition and Sources: The authors compile a primary survey dataset designed to evaluate AI-driven fraud detection adoption across Nigeria’s banking sector. The data originates from a cross-sectional study targeting a population of 24 licensed Deposit Money Banks, with five institutions selected through purposive sampling based on market capitalization, total assets, and customer base.

- Subset Details: The final collection comprises 47 valid questionnaire responses. Each participating bank contributes 10 senior staff members, creating a structured breakdown by department (40 percent IT, 26 percent fraud investigation, 34 percent risk management), gender (72 percent male, 28 percent female), and professional experience (less than 10 years, 10 to 20 years, and over 20 years).

- Data Usage and Processing: The authors utilize the dataset to run an Ordered Logistic Regression model that identifies key adoption drivers and barriers. The data is structured into demographic metadata and ordinal Likert scale responses for statistical modeling rather than machine learning training splits. Response distributions are aggregated to calculate regression coefficients for variables like management support, IT infrastructure, and implementation costs.

- Validation and Instrument Processing: The survey instrument follows a two-part structure that separates respondent background information from operational questions rated on a five-point Likert scale. The authors ensure construct validity through expert review and verify internal consistency using Cronbach's Alpha, retaining only items that meet a 0.72 reliability threshold before final analysis.

Method

The authors leverage an Ordered Logistic Regression (OLR) model to analyze the relationship between the adoption level of AI-driven fraud detection systems (AIFA) and various influencing factors. This approach is appropriate given that the dependent variable, AIFA, is measured on an ordinal scale, reflecting a natural ranking of adoption levels without assuming equal intervals between categories. The functional form of the model is expressed as:

AIFA=f(TMS,ITI,COI,REC,COM,PEF)where TMS represents top management support, ITI denotes IT infrastructure, COI stands for cost of implementation, REC refers to regulatory compliance, COM indicates staff competency, and PEF represents perceived effectiveness.

In econometric form, the model is specified as:

\logit(P(Y=j))=αj+β1TMS+β2ITI+β3COI+β4REC+β5COM+β6PEFHere, P(Y=j) denotes the cumulative probability that the response variable Y, representing the level of AI fraud detection system adoption, falls in category j or below. The parameters αj represent the cut-off points for each category, while β1 through β6 are the coefficients associated with the respective explanatory variables. The model estimates how changes in each predictor affect the odds of being in a higher category of adoption, thereby identifying the factors that significantly influence the degree of AI adoption in fraud detection.

[[IMG:]]

Experiment

The evaluation began with reliability testing and chi-square analysis to validate the measurement instrument and confirm that institutional scale significantly influences AI adoption patterns. Ordered logistic regression modeling was subsequently employed to isolate the core organizational drivers, validating that executive commitment, robust IT infrastructure, regulatory alignment, workforce expertise, and perceived system utility positively facilitate implementation, whereas high financial barriers deter adoption. Diagnostic testing further confirmed the statistical appropriateness of the analytical framework, collectively establishing that institutional capacity and leadership alignment are the foundational determinants of successful AI integration for fraud detection in the banking sector.

The authors conduct a chi-square test to examine the relationship between bank size and the level of AI adoption, finding a statistically significant association. The results indicate that larger banks are more likely to adopt AI technologies compared to smaller banks, suggesting differences in resources and digital maturity influence adoption levels. There is a statistically significant association between bank size and the level of AI adoption. Larger banks are more likely to adopt AI technologies compared to smaller banks. The association is statistically significant, indicating that bank size influences AI adoption levels.

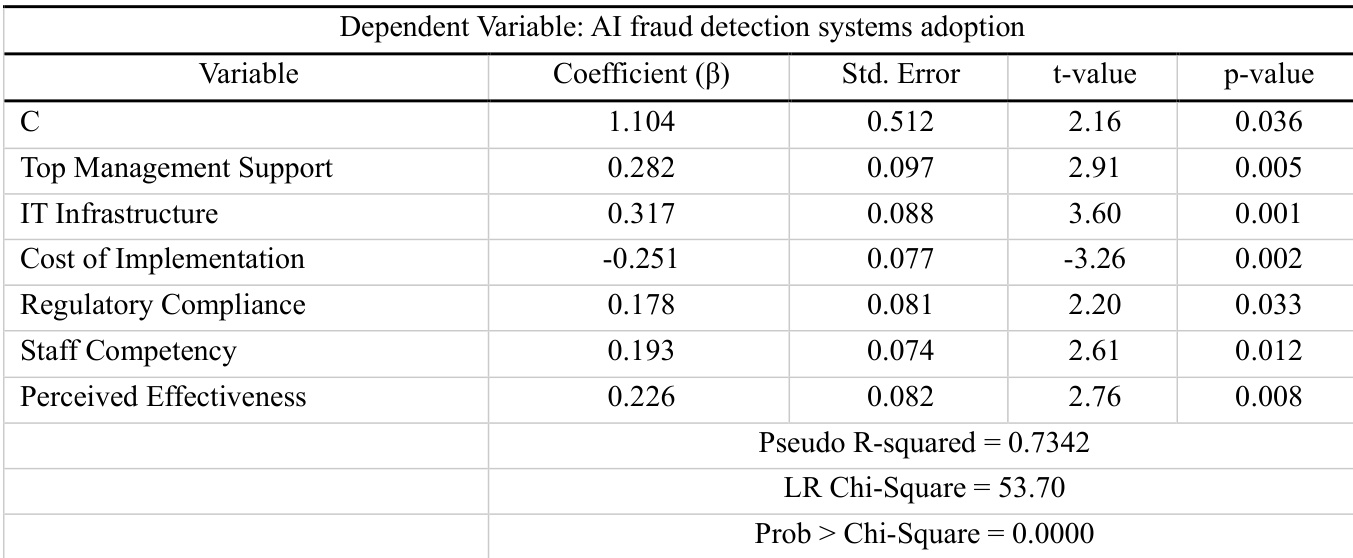

The authors analyze factors influencing the adoption of AI fraud detection systems in Nigerian banks using a regression model. Results show that top management support, IT infrastructure, regulatory compliance, staff competency, and perceived effectiveness have positive and significant impacts, while implementation cost has a negative and significant impact on adoption levels. Top management support, IT infrastructure, regulatory compliance, staff competency, and perceived effectiveness positively influence AI fraud detection adoption. Implementation cost negatively impacts AI fraud detection adoption. The regression model explains a substantial portion of the variance in AI adoption levels.

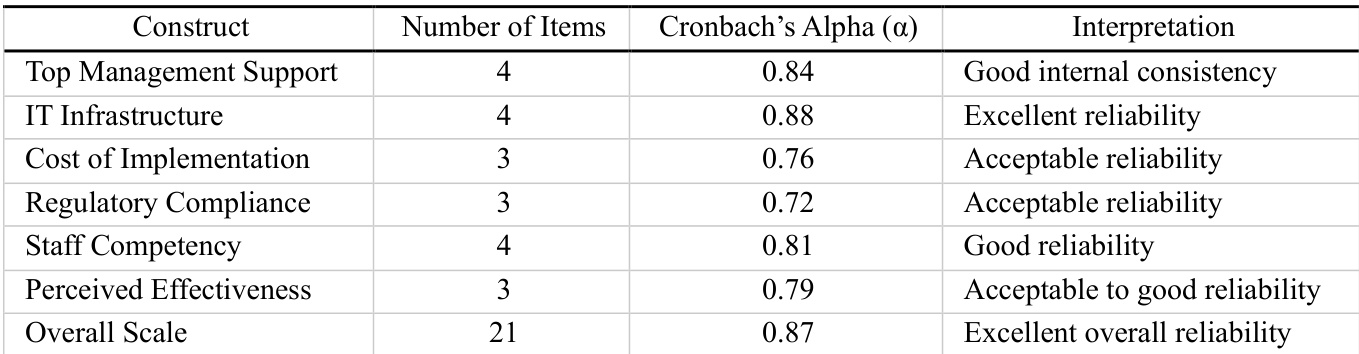

The authors assess the internal consistency of survey constructs using Cronbach's Alpha, indicating that most constructs demonstrate good to excellent reliability. The overall scale, composed of multiple items, shows strong reliability, supporting the robustness of the measurement framework used in the study. Most constructs exhibit good to excellent internal consistency, with Cronbach's Alpha values above 0.7 for the majority. The overall scale, combining multiple items, shows excellent reliability, indicating strong measurement consistency. Constructs like cost of implementation and regulatory compliance show acceptable reliability, suggesting adequate internal consistency for these variables.

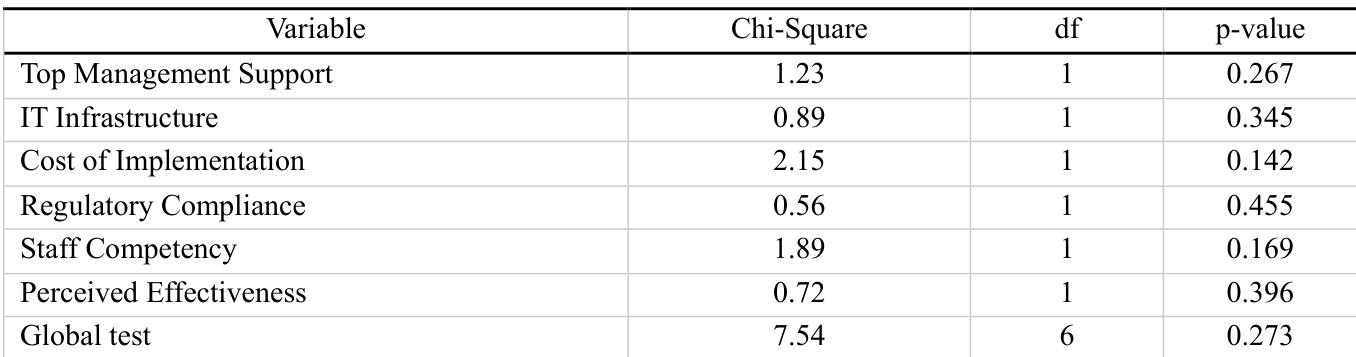

The authors analyze factors influencing the adoption of AI-driven fraud detection systems in Nigerian banks using statistical tests. Results from a chi-square test show no significant associations between the variables and adoption levels, while a global test confirms the appropriateness of the regression model used. The findings suggest that certain factors such as top management support and IT infrastructure may influence adoption, but the statistical significance of these relationships varies. The chi-square test results indicate no statistically significant associations between the variables and AI adoption levels. The global test supports the validity of the ordered logistic regression model used in the analysis. The analysis highlights that factors like top management support and IT infrastructure are considered important, though their statistical significance is not confirmed by the chi-square test.

The research employs chi-square tests, regression modeling, and reliability assessments to evaluate the organizational drivers and measurement validity of AI adoption in banking, particularly for fraud detection systems. The statistical analyses validate that larger institutions adopt AI more readily due to superior resources and digital maturity, while successful implementation hinges on executive support, robust IT infrastructure, regulatory compliance, staff competency, and perceived effectiveness, with high costs serving as a primary deterrent. Although bivariate tests show limited direct associations, the validated regression framework confirms that these multifaceted factors collectively shape adoption decisions. Additionally, reliability assessments substantiate the methodological rigor of the study, demonstrating strong internal consistency across all survey constructs.